Table Of Content

San Bernardino County was listed as the most affordable in Southern California in the report. Also, if a buyer has a co-signer, like a parent, they may have an advantage. Kochova said the banks are motivated right now to get buyers into homes, especially since inventory is slowly creeping up and interest rates are staying low. Orange County buyers have an even higher minimum income to meet, at a jarring $162,000.

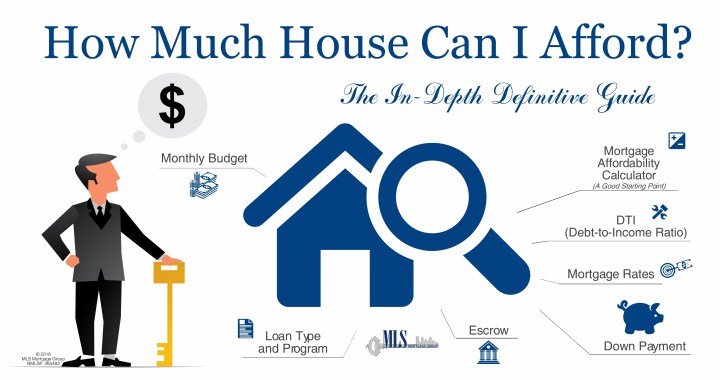

Start with the 28/36 rule

Some of the best include increasing your income, decreasing your monthly payment by making a bigger down payment, and moving to a more affordable neighborhood. First, you’ll need to do the hard work of saving up $80,000 in cash as a 20% down payment. Or if you already own a home, make sure you have enough equity to pay off your current mortgage and cover your down payment when you sell it. A recent PYMNTS/LendingClub survey found that 49% of people who make $100,000 or more are still living paycheck-to-paycheck.

Specialized Home Buying Programs

Most financial advisors agree that people should spend no more than 28 percent of their gross monthly income on housing expenses, and no more than 36 percent on total debt. The 28/36 percent rule is a tried-and-true home affordability rule of thumb that establishes a baseline for what you can afford to pay every month. That means your mortgage payment should be a maximum of $1,120 (28 percent of $4,000), and your other debts should add up to no more than $1,440 each month (36 percent of $4,000). You’ll need to determine a budget that allows you to pay for essentials like food and transportation, wants like entertainment and dining out, and savings goals like retirement.

Great Credit and Low Interest Rate

This can mean private mortgage insurance (PMI), which is an added monthly charge to secure your loan. If you don’t have enough money for a down payment, many lenders will require that you have mortgage insurance. You’ll have to pay your monthly mortgage as well as a monthly insurance payment, so it’s not the best option if your budget is tight.

Researching neighborhoods and planning for commuting times can help in making a successful transition. Additionally, embracing the diverse culture and exploring different parts of the city can lead to discovering hidden gems and building a connection to the community. "COVID relief policies bolstered the economy, leading to boosted stock prices, real estate and savings," Murray told CBS MoneyWatch. "These conditions were especially favorable for the wealthiest of Americans, who experienced dramatic income increases, especially considering the fact that many companies saw record profits." At the same time, the nation's top-earning households are gaining a greater share of income, fueling rising income inequality, Census data shows.

Perhaps more importantly, however, you avoid putting yourself at the limits of your financial resources if you choose a house with a price lower than your maximum. But beyond that you’ve got to think about your lifestyle, such as how much money you have leftover for travel, retirement, other financial goals, etc. You might find that you don’t want to buy the most expensive home that fits in your budget.

Savings and down payment

Community reviews are used to determine product recommendation ratings, but these ratings are not influenced by partner compensation.

So yes, hypothetically you should be able to afford a $400,000 home. However, $500,000 would be pushing it – the same loan on a house of that price would equate to $2,528 in monthly principal and interest payments, which exceeds your limit of $2,333. Mortgage insurance protects the mortgage lender against loss if a borrower defaults on a loan. Private mortgage insurance (PMI) is required for borrowers of conventional loans with a down payment of less than 20%.PMI typically costs between .05% to 1% of the entire loan amount.

Singer points out that even with this more forgiving calculation, your debt-to-income ratio still cannot surpass 36%. Many experts say the upper limit is actually two percentage points higher at 30%, which gives you a little more buying power. Washington state has seen the most dramatic growth in what it takes to be rich in recent years, according to the report. In 2017, a salary of about $378,000 would land you in the 5% club. By 2022, the salary it takes to stay at that level is more than $544,000. Meanwhile, joining the 5% of earners requires considerably more in many Eastern states, with Connecticut's threshold at $656,438 and New York at $621,301, the study found.

How Much House Can I Afford On A $130K Salary? - Bankrate.com

How Much House Can I Afford On A $130K Salary?.

Posted: Wed, 04 Oct 2023 07:00:00 GMT [source]

A higher credit score will get you a lower interest rate, and the lower your interest rate, the more you can afford to borrow. The longer you can stay in a home, the easier it is to justify the expenses of closing costs and moving all your belongings — and the more equity you’ll be able to build. Some programs, such as the zero-down USDA mortgage, have income limits on who can qualify. The USDA program caps income at 115% of the area median income (AMI).

We do not include the universe of companies or financial offers that may be available to you. Naturally, the lower your interest rate, the lower your monthly payment will be. Want a quick way to determine how much house you can afford on a $40,000 household income?

This commonly used guideline states that you should spend no more than 28 percent of your income on your housing expenses, and no more than 36 percent on your total debt payments. This borrower could afford up to $394,200 while staying within the 28% rule. This would mean a monthly payment of $1807 with an additional $526 in taxes and fees for a total of $2,333.

If you’re getting a conventional loan with less than 20% down and will have to pay private mortgage insurance (PMI), try to minimize this expense. The larger your down payment and the better your credit score, the lower your PMI rate and the fewer years you’ll have to pay it for. Lenders prefer to see an 80/20 LTV, which requires a 20 percent down payment. Down payment & closing costsNerdWallet's ratings are determined by our editorial team.

How much of that $100,000 salary have you been able to squirrel away in savings? Shifting your money into a high-yield savings account can help accelerate your savings efforts. Conventional loans can come with down payments as low as 3%, although qualifying is a bit tougher than with FHA loans. Our partners cannot pay us to guarantee favorable reviews of their products or services. According to Zillow, the median U.S. home value is $339,084, which should be close to your price range’s sweet spot once you earn a six-figure salary.

In order to determine how much mortgage you can afford to pay each month, start by looking at how much you earn each year before taxes. Then take your annual income and divide by 12 to determine your monthly income. What if you have a student loan in deferment or forbearance and you’re not making payments right now?

The more quotes you get, the greater possibility that you can save thousands of dollars over the life of your loan. A good answer would be a home that you won’t regret buying and one that won’t have you wanting to upgrade in a few years. As much as mortgage brokers and real estate agents would love the extra commissions, getting a mortgage twice and moving twice will cost you a lot of time and money. Loan requirements for cash reserves usually range from zero to six months. But even if your lender allows it, exhausting your savings on a down payment, moving expenses and fixing up your new place is tempting fate. Fees depend on how many amenities the community has, how many services it requires, and how much upkeep it needs.

No comments:

Post a Comment